With the blink of an eye, one year flew past. Focus of 2021 is still much about COVID-19, not the original virus, but its mutation. We have the Delta version, and now the Omicron variant, which is less serious, but more infectious. Countries are transiting to endemic states, though border controls for international leisure are pretty much still in place, with the exception of vaccinated travel lanes for business. Hospitality sector and airlines are estimated to return to pre-COVID levels in the next 2 years, depending on when this pandemic wave is over. Experts are currently debating if the Omicron variant will be the last of COVID-19, that will ensure its survival among us humans.

For me, some big changes are happening to my company. For one, they will be implementing the flexi-work arrangement, which employees are only required to return to office 2 days out of a week of your choice. For the rest of the 3 days, employees are to Work From Home. We have also just shifted to a new smaller office unit and the new pantry looks exciting, with better drinks and snacks stock up. Organization too need to adopt to the new norms.

DJI ended at 36338, an increase of 2495 points (+7.37%) compared to 3Q 2021. For Singapore, STI ended at 3123, an increase of 37 points (+1.19%) compared to last quarter. Singapore market has lagged DJI again, not matching the growth seen at the USA market. For Q4, the investor community are pretty hyped that the world seems to be moving out from the shadows of COVID. Airline and hospitality sector are hitting their annual highs. Government are looking at finally ending budget stimulus and raising interest rates as economy are returning to their pre-COVID levels. USA in particular, are increasingly likely to start raising interest rates in 2022.

With 2021 drawing to a close, it is time for the annual review against my 3 year plan (Next 3 years (2020 - 2022) Investment Plan) set back in Dec 2019. Below are my result:

Original 2020-2022 plan:

- 50% Equity, 50% Reits/Trusts

- Portfolio Dividend Yield to be 3.50% in 2020, 4.20% in 2021, 4.80% in 2022.

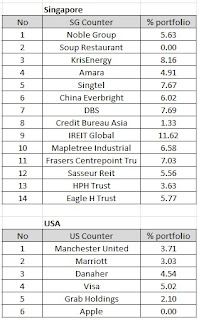

- 59.81% Equity, 40.19% Reits/Trusts

- 81.60% SG Equity, 18.40% USA Equity

- Portfolio Yield at 3.07% in 2021 (+0.42% from 2020, but miss 2021 4.20% target)

Below is my end 2021 portfolio snapshot:

Total dividend received in 2021: $4,335.27 (~$361.27/month)

2021 continues to be a challenging year. All I can do is to have patience and wait for the norms to return, so that investment can bear fruits at the time when I bought them at their pandemic lows. Thank God for blessing my family with good health and providing all that we need. Thank God that I still managed to grow my overall portfolio value and dividend returns. We need to start planning early for retirement passive income, which requires time to build up slowly brick by brick. Now, enough talking, below are my transaction for this quarter:

Transaction 1: Sold 1 batch Marriott shares in October.

Time to cash in as the stock raise to $160. Cant resist the high price and decide to lock in some profits. The next batch to sell will probably be the time when Marriott restart their dividend and share buybacks. I estimate by then, the price should hit $185. Lets see if I am spot on.

Transaction 2: Bought 1 batch Danaher shares in October.

As the community are looking at re-opening of economy in October, medical shares got battered as they deem COVID are soon to be over and there will be lesser demand for COVID testing and related services. They are proved wrong a few weeks later with the Omicron emergence. Anyway, bought in this counter for the long term during the price drop for the company culture of using free cash flow to continue investing and acquire companies for growth.

Transaction 3: Bought 1 batch Visa shares in November.

With Omicron ravaging countries rapidly in November, financial counters took a hit as countries re-impose lockdowns and investors start selling their position and took profits accumulated over the past few months. For me, I bought in more shares for the long term during the dip due to Visa generous free cash flow and share buyback program. With lesser supply, price are bound to rise over time. Simple theory.

Transaction 4: Bought 2 batch Grab shares in November.

What excitement to see our fellow SG company debut in NASDAQ? Well, I personally believe Grab will be able to start making a profit after further fine-tuning their business model. Imagine the vast potential Grab can tap once they start monetizing their Ad outreach through their app and the start of their digital bank partnership with Singtel in 2022? Well, we will have more clarity once they start reporting their first financial result since listing. In the mean time, I just took some position when the share tanks.

Transaction 5: Bought 1 batch Singtel shares in December.

Continue accumulating Singtel shares in the face of price weakness due to pandemic and international border closure. Once things start to normalize, Singtel price should recover to at least $3.00. Anyway, India Bharti Airtel has bottom out and start turning in a profit after 5 years of brutal price war locally. This should help Singtel with its underlying profit and resumption of generous dividend.

Transaction 6: Bought 1 batch DBS shares in December.

Continue accumulating DBS shares until USA starts raising interest rates. I believe current price of $32 still do not reflect DBS true strength, after they have acquired stakes in China Shenzhen Rural Commercial Bank in April this year and taken over India Lakshmi Vilas Bank in Nov 2020. Personally, I believe DBS will make record profits for the next 4 quarter at least once interest rates begin to rise.

Transaction 7: Bought 1 batch China Everbright Water shares in December.

Continue accumulating China Everbright Water shares for their annual increase in dividend, yearly winning bids for government projects and most importantly, China push for sustainability. With this, wastewater treatment will be one of the main country focus which I cannot see a reason how this company can run into trouble, with such a strong backing from the parent company listed in HKSE. With the current $0.305 price, this work out to be a dividend yield of 6.55%.

Well, that is all for now. See you all in Q1 2022 update and thank you for reading thus far (I know this is such a long posting). Wishing everyone a Happy New Year. Stay healthy, stay safe, stay mask up and may God Bless you with a good year ahead~

No comments:

Post a Comment